IFRS 9 - Financial Instruments

Vertex Learning Solutions

Vertex Learning Solutions

Financial Instruments From Basics - Classification, Recognition and Measurement

IFRS -9 - Financial Instruments:

Let us start by looking at the definition of a financial instrument. A financial instrument is a contract that gives rise to a financial asset of one entity and a financial liability or equity instrument of another entity. Financial instruments are covered in three different standards by IASB which includes the following:

- IAS 32 deals with the classification of financial instruments and their financial statement presentation.

- IFRS 7 deals with the disclosure of financial instruments in financial statements.

- IFRS 9 is concerned with the initial and subsequent measurement of financial instruments.

In this article we are going to understand details regarding financial asset ,financial liability and compound instruments.

IAS 32 provides rules on classifying financial instruments. The issuer of a financial instrument must classify it as a financial liability or equity instrument on initial recognition according to its substance. However our focus in this article is only upon IFRS 9 which in itself is a detailed standard and covers various aspects affecting financial statements. IFRS 9 Financial Instruments is the IASB’s replacement of IAS 39 Financial Instruments: Recognition and Measurement. It is effective for annual periods beginning on or after 1 January 2018 with early application permitted.

This Standard includes requirements for

- Recognition and measurement

- Impairment

- Derecognition

- General hedge accounting.

As per the definition described above financial instruments are contracts, and therefore principally financial assets, financial liabilities and equity instruments are going to be pieces of paper.

IFRS 9 requires an entity to recognize a financial asset or a financial liability in its statement of financial position when it becomes party to the contractual provisions of the instrument. At initial recognition, an entity measures a financial asset or a financial liability at its fair value plus or minus, in the case of a financial asset or a financial liability not at fair value through profit or loss, transaction costs that are directly attributable to the acquisition or issue of the financial asset or the financial liability.

We need to remember that the accounting treatment of interest, dividends, losses and gains relating to a financial instrument follows the treatment of the instrument itself.

Financial Liabilities

Initial recognition of financial liabilities

At initial recognition, financial liabilities are measured at fair value.

- If the financial liability will be held at fair value through profit or loss, transaction costs should be expensed to the statement of profit or loss.

- If the financial liability will not be held at fair value through profit or loss, transaction costs should be deducted from its carrying amount.

Subsequent measurement of financial liabilities

The subsequent treatment of a financial liability is that they can be measured at either:

- Amortised cost

- Fair value through profit or loss.

Financial Assets

There are two types of financial asset (equity and debt instruments), which can be further split into different categories.

(a) Equity investments

Equity instruments are likely to be shares that have been purchased in a company, but not enough to give the investee significant influence (associate), control (subsidiary) or joint control (joint venture).There are two options here, depending on the intention of the entity. The default category is fair value through profit or loss (FVPL) and the other one being fair value through other comprehensive income (FVOCI)

(b) Debt instruments:

These are usually bonds or loan notes, or other instruments which are likely to carry interest and a capital element of repayment. The treatment of the debt instrument depends on the intention of the entity, and there are three options for categorizing debt instruments.

- Fair value through other profit or loss (FVPL)

- Amortized cost

- Fair value through other comprehensive income (FVOCI)

Now let’s see these classifications in detail. When an entity first recognizes a financial asset, it classifies it based on the entity’s business model for managing the asset and the asset’s contractual cash flow characteristics, as follows:

- Amortized cost—a financial asset is measured at amortized cost if both of the following conditions are met:

- The asset is held within a business model whose objective is to hold assets in order to collect contractual cash flows; and

- The contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding.

- Fair value through other comprehensive income—financial assets are classified and measured at fair value through other comprehensive income if they are held in a business model whose objective is achieved by both collecting contractual cash flows and selling financial assets.

- Fair value through profit or loss—any financial assets that are not held in one of the two business models mentioned are measured at fair value through profit or loss.

We should note that only when an entity changes its business model for managing financial assets it must reclassify all affected financial assets.

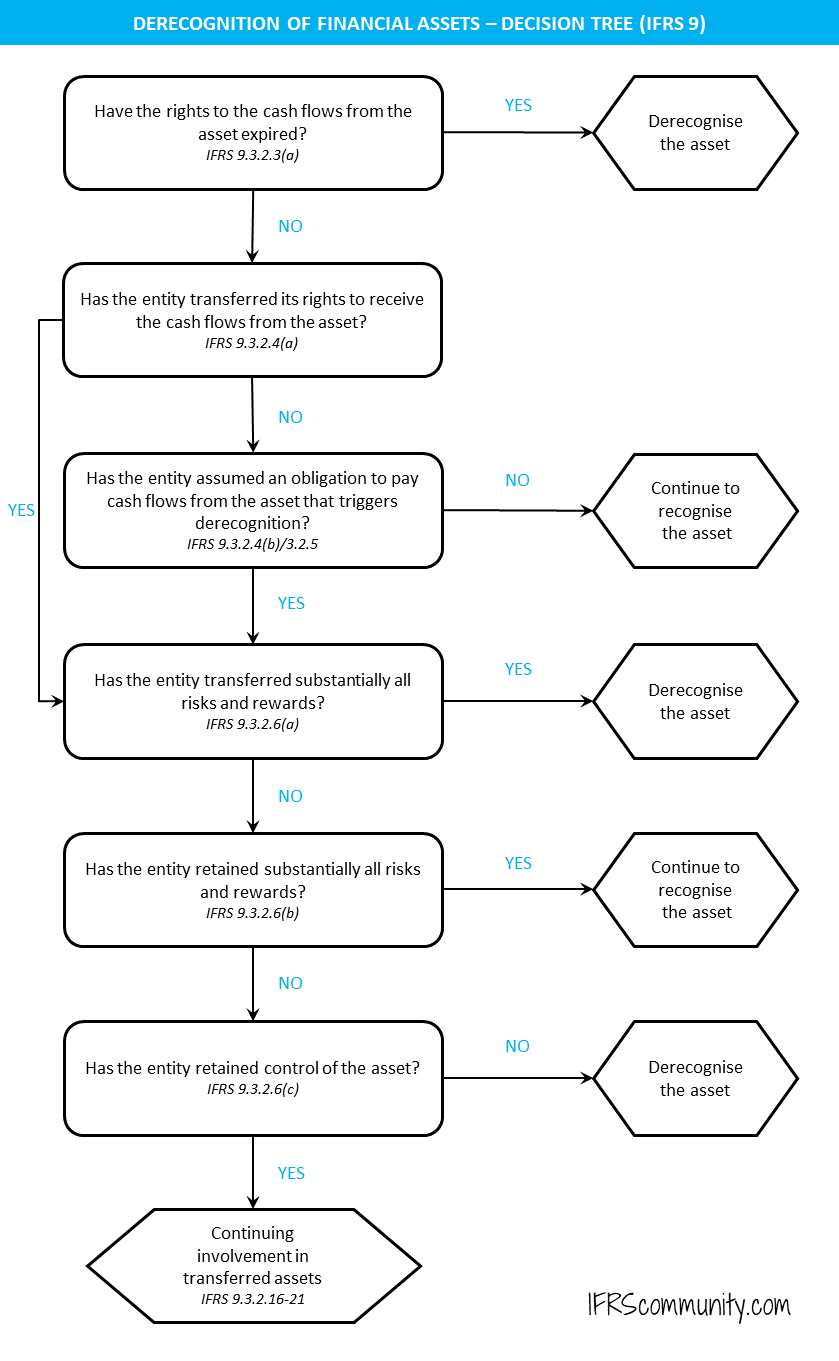

Derecognition:

Derecognition criteria for financial assets are summarised in the decision tree below. This is a very useful framework that helps go through the discussion that follows.

As we have looked into IFRS-9 basic criteria now here is a brief summary regarding the impact on financial statement of the chosen treatment of financial assets at all stages of recognition measurement and derecognition.

(Click for complete IFRS 9 Online Course)

|

Category |

Impact on Financial Statements |

|

Amortized Cost |

The asset is measured at the amount recognized at initial recognition minus principal repayments, plus or minus the cumulative amortization of any difference between that initial amount and the maturity amount, and any loss allowance. Interest income is calculated using the effective interest method and is recognized in profit and loss. Changes in fair value are recognized in profit and loss when the asset is derecognized or reclassified. |

|

FVOCI |

The asset is measured at fair value. Loans and receivables. Interest revenue, impairment gains and losses, and a portion of foreign exchange gains and losses, are recognized in profit and loss on the same basis as for Amortized Cost assets. Changes in fair value are recognized initially in Other Comprehensive Income (OCI). When the asset is derecognized or reclassified, changes in fair value previously recognized in OCI and accumulated in equity are reclassified to profit and loss on a basis that always results in an asset measured at FVOCI having the same effect on profit and loss as if it were measured at Amortized Cost. Investments in equity instruments. Dividends are recognized when the entity’s right to receive payment is established, it is probable the economic benefits will flow to the entity and the amount can be measured reliably. Dividends are recognized in profit and loss unless they clearly represent recovery of a part of the cost of the investment, in which case they are included in OCI. Changes in fair value are recognized in OCI and are never recycled to profit and loss, even if the asset is sold or impaired |

|

FVPL |

The asset is measured at fair value. Changes in fair value are recognized in profit and loss as they arise |

Reclassification of Financial Assets and Liabilities

In general, reclassifications of financial assets are accounted for prospectively under IFRS 9; i.e., they do not result in restatements of previously recognized gains, losses or interest income. (Click for complete IFRS 9 Online Course)

|

From |

To |

Requirement |

|

Amortized Cost |

FVPL |

Measure fair value at reclassification date and recognize difference between fair value and Amortized Cost in profit and loss |

|

FVPL |

Amortized Cost |

Fair value at the reclassification date becomes the new gross carrying amount |

|

Amortized Cost |

FVOCI |

Measure fair value at reclassification date and recognize any difference in OCI |

|

FVOCI |

Amortized Cos |

Cumulative gain or loss previously recognized in OCI is removed from equity and applied against the fair value of the financial asset at the reclassification date |

|

FVPL |

FVOCI |

Asset continues to be measured at fair value but subsequent gains and losses are recognized in OCI rather than profit and loss |

|

FVOCI |

FVPL |

Asset continues to be recognized at fair value and the cumulative gain or loss previously recognized in other comprehensive income is reclassified from equity to profit and loss |

Expected Credit Loss Framework

Under IFRS 9, financial assets are classified according to the business model for managing them and their cash flow characteristics. In essence, if these 3 conditions are met then the financial asset is held at amortised cost.

- A financial asset is a simple debt instrument such as a loan,

- The objective of the business model in which it is held is to collect its contractual cash flows (and generally not to sell the asset) and

- Those contractual cash flows represent solely payments of principal and interest,

The ECL framework is applied to those assets and any others that are subject to IFRS 9’s impairment accounting, a group that includes lease receivables, loan commitments and financial guarantee contracts. Under IFRS 9’s ECL impairment framework, however, banks are required to recognise ECLs at all times, taking into account past events, current conditions and forecast information, and to update the amount of ECLs recognised at each reporting date to reflect changes in an asset’s credit risk. It is a more forward-looking approach than its predecessor and will result in more timely recognition of credit losses.

IFRS 9 says that the following events may suggest the asset is credit-impaired:

- significant financial difficulty of the issuer or the borrower

- a breach of contract, such as a default

- the borrower being granted concessions

- it becoming probable that the borrower will enter bankruptcy

Three Stages of Impairment

Impairment of loans is recognised – on an individual or collective basis – in three stages under IFRS 9:

Stage 1 – When a loan is originated or purchased, ECLs resulting from default events that are possible within the next 12 months are recognised (12-month ECL) and a loss allowance is established. On subsequent reporting dates, 12-month ECL also applies to existing loans with no significant increase in credit risk since their initial recognition. Interest revenue is calculated on the loan’s gross carrying amount (that is, without deduction for ECLs).

Stage 2 – If a loan’s credit risk has increased significantly since initial recognition and is not considered low, lifetime ECLs are recognised. The calculation of interest revenue is the same as for Stage 1.

Stage 3 – If the loan’s credit risk increases to the point where it is considered credit-impaired, interest revenue is calculated based on the loan’s amortised cost (that is, the gross carrying amount less the loss allowance). Lifetime ECLs are recognised, as in Stage 2.

Impairment Reversals

At each reporting date, the loss allowance is recalculated. It may be that the allowance was previously equal to lifetime credit losses but now, due to reductions in credit risk, only needs to be equal to 12-month expected credit losses. As such, there may be a substantial reduction in the allowance required. Gains or losses on remeasurement of the loss allowance are recorded in profit or loss.

Compound Instruments

It is a financial instrument that has characteristics of both equity and liabilities. An example would be debt that can be redeemed either in cash or in a fixed number of equity shares.

IAS 32 requires compound financial instruments be split into two components:

- a financial liability (the liability to repay the debt holder in cash)

- an equity instrument (the option to convert into shares).

These two elements must be shown separately in the financial statements.

On initial recognition, a compound instrument must be split into a liability component and an equity component:

- The liability component is calculated as the present value of the repayments, discounted at a market rate of interest for a similar instrument without conversion rights.

- The equity component is calculated as the difference between the cash proceeds from the issue of the instrument and the value of the liability component.

(Click for complete IFRS 9 Online Course)

References:

https://www2.deloitte.com

https://www.accaglobal.com

https://www.ifrs.org

{kind=link}